We would all like to manage our money better. I used to get stuck looking at my balance and trying to figure out whether certain bills had come out and whether I would have enough money to cover the next bill. Now I don’t have that problem, due to a banking system that is known as piggy banking.

We would all like to manage our money better. I used to get stuck looking at my balance and trying to figure out whether certain bills had come out and whether I would have enough money to cover the next bill. Now I don’t have that problem, due to a banking system that is known as piggy banking.

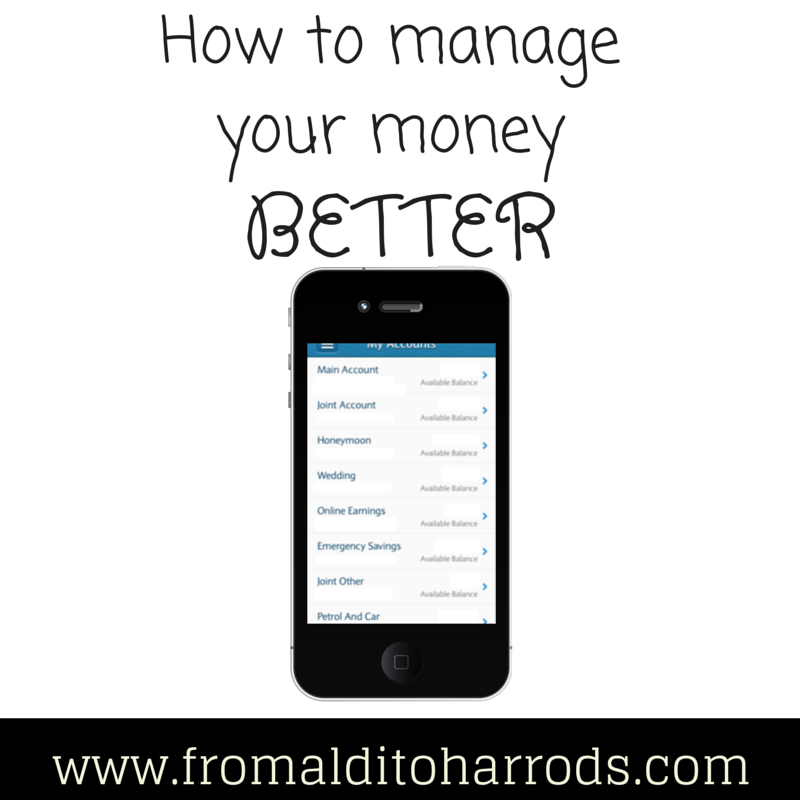

Piggy banking is where I take my income and divide it into separate “pots”, depending on what it needs to be spent on. You can use cash and envelopes, or what I do is have different bank and savings accounts. When I log into my online banking, I am greeted with lots of accounts. In fact, there are 12 in total. As you can see, I have my “main account” which is just my normal current account with a debit card, and our joint account, which again, comes with a debit card. Everything else is either an e-savings account, an everyday savers account or my ISA. None of these other accounts came with a debit card, but I can access my cash in any of them instantly. It is important to note that whilst these are technically savings accounts, I am not using them as savings accounts – they have awful interest rates and I’m not saving long term in them.

Every month, on pay day, I divide my money between each account according to my predicted spending. The best example of this is my “petrol and car” account, as I pay for my fuel with a credit card (for Tesco Clubcard points) and then pay it off once a month. Before paying it off, I simply transfer the money from my “petrol and car” account into my normal account, using the Barclays Mobile App.

It also helps you to budget for annual costs. I know roughly how much my car insurance is, as well as the other annual car related costs such as MOT, servicing and new tyres. I add this all up, divide it by 12 (or you can do it by 52 if you are paid weekly, 13 if paid every 4 weeks) and make sure to put that amount into my “petrol and car” pot. Then once those costs roll around, the money is there waiting, instead of spent because it was sat in my current account and I thought it was mine to spend. There are plenty of other annual costs that you can use this method for:

- Christmas

- Birthdays

- Other gifts (wedding, christening, etc)

- Heating oil delivery

- Emptying septic tank

Whilst you can plan for certain expenses, you may still find yourself hit with a bill higher than you were anticipating. That is why it is a great idea to have an emergency fund, no matter how little you can save per month. Even £10 a month is a good start.

You could go one step further and separate your money even more – by allocating a certain amount for groceries, toiletries, clothes, etc. I found that this was too restrictive for me, so instead I leave a set amount of money in my current account to spend as I see fit, and for the joint account we have a weekly budget to cover groceries, toiletries, cleaning, meals out and any other household expenses.

You can set up some extra savings accounts by ringing your bank, in branch or applying online. They are free to open, and you just want really basic savings accounts – not to be tied in to anything, such as a withdrawal notice period.

I would love to hear from others as to how they manage their finances. Please leave a comment and let me know.

You might also like

Switch banks & make money

Switch banks & make money FairFX pre-paid currency card review & get a free card

FairFX pre-paid currency card review & get a free card Pay As You Go With Three

Pay As You Go With Three One month trial of Which? for just £1

One month trial of Which? for just £1 Switching bank accounts with TSB

Switching bank accounts with TSB Save money on taxi journeys with Uber and get £20 FREE

Save money on taxi journeys with Uber and get £20 FREE 6 Things To Do When You Can’t Pay This Month’s Bills

6 Things To Do When You Can’t Pay This Month’s Bills Make £10 a Day in July Challenge

Make £10 a Day in July Challenge

Jane Brown says

We have a separate account for bills. We set up a spreadsheet with the bills showing over 12 months, which works out how much per month needs to be allocated for the bills. That amount is automatically paid into the bills account just after my partner gets paid. It is my job to update it whenever a new bill is paid and make sure enough is allocated.

Julie says

Really practical tips – I agree that online money management makes life much simpler. I set aside my savings first after I’m paid, then I know that what’s left is OK for spending. Separate pots do work to help with that.